Picking Up The Tab 2015: Small Businesses Pay the Price for Offshore Tax Havens

Every year, corporations and wealthy individuals use complicated gimmicks to shift U.S. earnings to subsidiaries in offshore tax havens – countries with minimal or no taxes – in order to reduce their federal and state income tax liabilities by billions of dollars. While tax haven abusers benefit from America’s markets, public infrastructure, educated workforce, security and rule of law – all supported in one way or another by tax dollars – they continue to avoid paying for these benefits. Small business owners are hit twice by the effects of tax dodging by large multinational corporations. Since they almost never have the kind of subsidiaries in the Cayman Islands or armies of tax lawyers and accountants to exploit tax haven loopholes that their multinational rivals do, small businesses are routinely placed at a competitive disadvantage in the market place. In addition, small businesses, like average taxpayers, end up picking up the tab for offshore tax avoidance in the form of higher taxes, cuts to public services, or increases to the federal debt. This study examines the potential impact of corporate tax dodging on America’s small businesses.

Every year, corporations and wealthy individuals use complicated gimmicks to shift U.S. earnings to subsidiaries in offshore tax havens – countries with minimal or no taxes – in order to reduce their federal and state income tax liabilities by billions of dollars. While tax haven abusers benefit from America’s markets, public infrastructure, educated workforce, security and rule of law – all supported in one way or another by tax dollars – they continue to avoid paying for these benefits.

Small business owners are hit twice by the effects of tax dodging by large multinational corporations. Since they almost never have the kind of subsidiaries in the Cayman Islands or armies of tax lawyers and accountants to exploit tax haven loopholes that their multinational rivals do, small businesses are routinely placed at a competitive disadvantage in the market place. In addition, small businesses, like average taxpayers, end up picking up the tab for offshore tax avoidance in the form of higher taxes, cuts to public services, or increases to the federal debt.

This study examines the potential impact of corporate tax dodging on America’s small businesses.

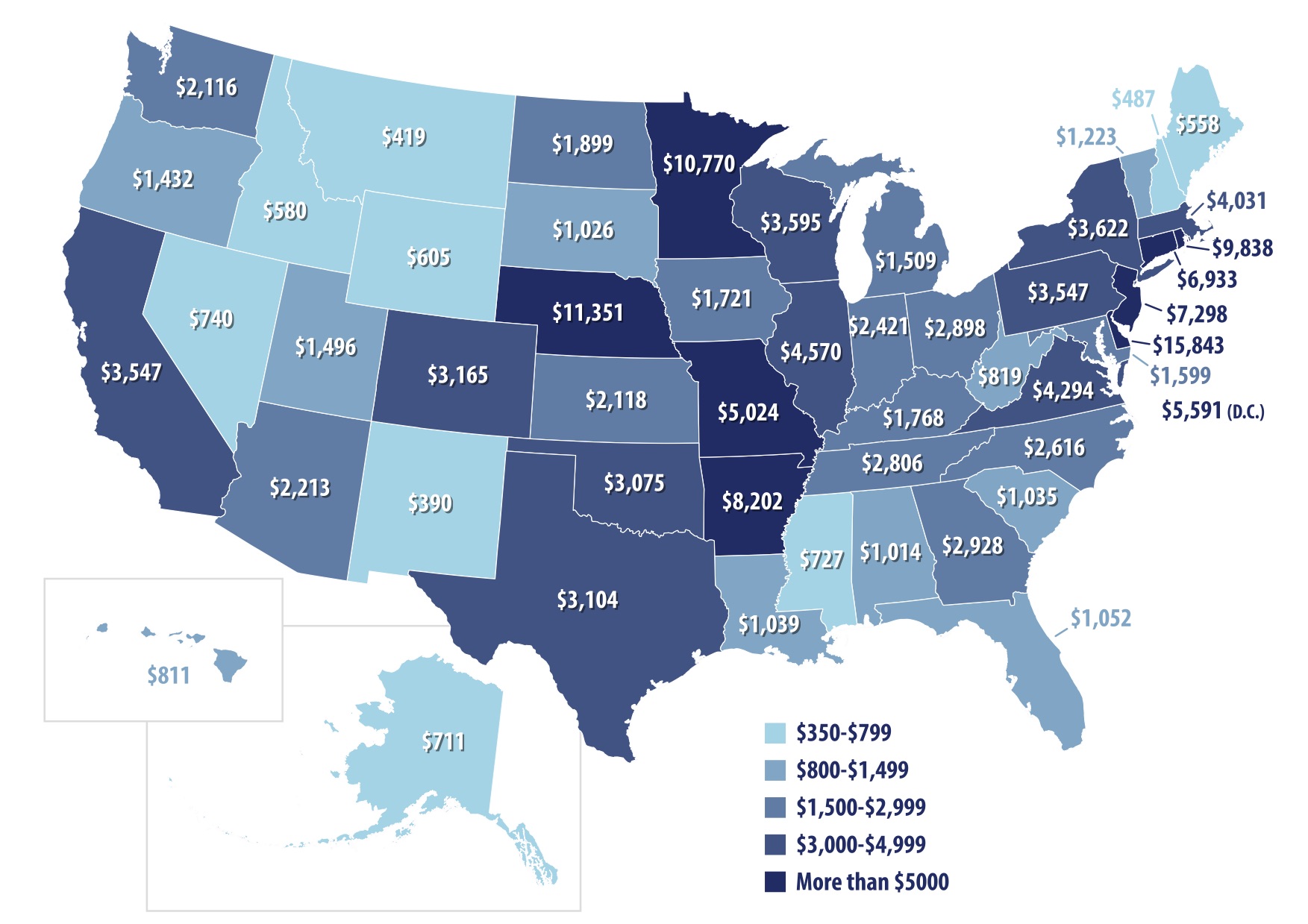

The United States loses approximately $110 billion in federal and state revenue each year due to corporations using tax havens to dodge taxes. In considering the impact of tax haven abuse, it is not possible to determine what portion of the lost revenue gets absorbed by program cuts or additional debt, but the analysis in this report shows the extent that tax responsibilities would be shifted in each state if the rest of the business sector picked up the tab – divided equally among the small businesses.

Each small business would need to pay an average of $3,244 in additional taxes if they were to pick up the full tab for income lost to corporations exploiting tax havens.

· Corporate tax haven abuse costs the federal government $90 billion in lost tax revenue. Every small business would need to pay an additional $2,684 in federal taxes to account for the revenue lost.

· Corporate tax haven abuse costs state governments an estimated $20 billion in lost tax revenue. Every small business would need to pay an additional $560 in state taxes to account for the revenue lost.

Figure ES-1. Picking Up the Tab: The Average Amount Small Business Owners in Each State Would Need to Pay to Make Up For State and Federal Revenue Lost To Offshore Tax Havens

Most of America’s biggest companies use tax havens to avoid tax obligations in the United States, including many that have taken advantage of government bailouts or rely on government contracts. At least 362 companies, making up 72 percent of the Fortune 500, maintained subsidiaries in tax haven jurisdictions as of 2013.[i]

· Pfizer, the world’s largest drug maker, paid no U.S. income taxes between 2010 and 2012 despite earning $43 billion worldwide. In fact, the corporation received more than $2 billion in federal tax refunds. In 2014, Pfizer operated 143 subsidiaries in tax haven countries and had $74 billion offshore and out of the reach of the Internal Revenue Service (IRS).

· Microsoft maintains five tax haven subsidiaries and stashed $92.9 billion overseas in 2014. If Microsoft had not booked these profits offshore, they would have owed an additional $29.6 billion in taxes.

· Citigroup, bailed out by taxpayers in the wake of the financial crisis of 2008, maintained 41 subsidiaries in tax haven countries in 2014, and kept $43.8 billion in offshore jurisdictions. If that money had not been booked offshore, Citigroup would have owed an additional $11.6 billion in taxes.

To restore fairness to the tax system, decision makers should end incentives for companies to book their income to offshore tax havens, close the most egregious loopholes, and increase transparency.

· End the ability of multinational corporations to indefinitely defer paying taxes on the profits they attribute to their foreign entities.

· Reject a “territorial” tax system, which would allow companies to temporarily shift profits to tax haven countries, pay minimal tax under those countries’ laws, and then bring the profits back to the United States tax-free.

· Put an end to the “check-the-box” rule, which currently allows multinational companies to make inconsistent claims about their corporate status. To maximize their tax advantage, corporations can currently tell one country that they are one type of entity while telling another country that the same entity is something else entirely.

· Stop companies from deducting interest expenses from their U.S. tax liability when that interest is paid to a foreign affiliate, a practice known as a form of “earnings stripping” that makes U.S. income appear to disappear.

· Shrink the ability for corporations to invert, or merge with an oftentimes smaller foreign entity and artificially re-designate their headquarters abroad to lower their tax bill.

· Reduce the incentive for corporations to license intellectual property (for example, patents and trademarks) to shell companies in tax haven countries before paying inflated – and tax-deductible – fees to use them in the United States.

· Treat the profits of publicly traded “foreign” corporations that are managed and controlled in the United States as domestic corporations for income tax purposes.

· Require multinational corporations to report their profits with a list of how their other profits were designated to each other nation, also known as “country by country reporting.”

· Equip the Department of Treasury with the enforcement power it needs to stop tax haven countries and their financial institutions from impeding tax collection in the United States.

· Require all companies to disclose their tax liability on their untaxed foreign profits – 55 of the Fortune 500 companies already do so, while the rest maintain it is not possible to calculate this number[ii].

[i] Dan Smith, Steve Wamhoff, and Richard Phillips, U.S. PIRG Education Fund, Offshore Shell Games: The Use of Offshore Tax Havens by the Top 100 Publicly Traded Companies, July 2014.

[ii] Dan Smith, Steve Wamhoff, and Richard Phillips, U.S. PIRG Education Fund, Offshore Shell Games: The Use of Offshore Tax Havens by the Top 100 Publicly Traded Companies, July 2014.